ASID Interior Design Billings Index (IDBI) December 2021

Billings, Inquiries, and Outlook Increase in December to End 2021 with Positive Momentum; Employment Levels for Both Interior Design and Architecture Services Fully Recovered

- The interior design industry concludes 2021 on an upbeat note as all three indices (Billings, Inquiries, and Six-Month Outlook) recorded monthly increases in December, signaling cautious optimism as we head into 2022. Even though the amount of uncertainty in today’s economy is high, the profession continues to find ways to be more resilient.

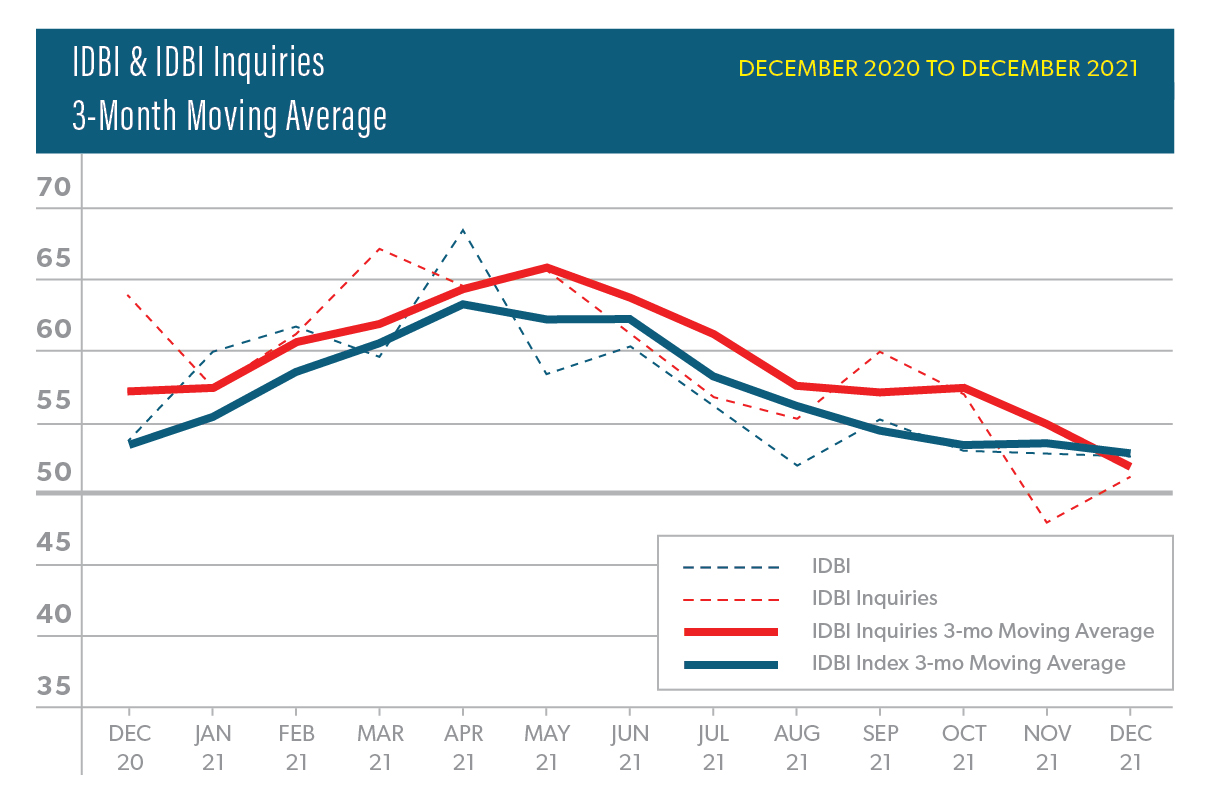

- Billings index* increased 0.3 points to 52.8 for December, reversing a downward trend over the last two months.

- The index grows its streak to 18 consecutive months in expansion (i.e., above 50).

- Even though the three-month moving average decreased slightly by 0.3 points to 52.8, this still indicates positive quarterly momentum for billings.

- Geographically, the South (58.1) continues to be the strongest region with regards to billings while the West (48.3) slides back into contraction territory with a three-month moving average below 50 (Midwest: 53.9; Northeast: 52.7).

- Inquiries index* rises 3.0 points to 51.0, returning to expansion after a quick, one-month departure in November (48.0).

- The three-month moving average decreased 2.9 points to 51.9, but, similar to the Billings index, it remains above 50, signifying positivity for future projects.

- The six-month outlook for interior design business experienced the largest change month-over-month among the three indices for December, increasing 4.8 points to 60.9.

- Panelists cite that the outlook could change based on two major factors: 1) the severity of COVID-19 and its variants and 2) how long it takes to resolve current supply chain issues.

- When asked about their sales outlook for 2022, panelists were three times more likely to indicate a ‘Strong’/‘Very strong’ stance vs a ‘Negative’/‘Very negative’ one (42% vs 14%).

- Billings index* increased 0.3 points to 52.8 for December, reversing a downward trend over the last two months.

Important Economic Indicators

- Employment Updates:

- As of December 2021, overall employment has recovered 18.8M jobs or 91% of the jobs lost from March 2020.

- As of November 2021, both Interior Design and Architectural services have completely recovered all the jobs lost from March 2020.

- However, the interior design industry is still 2.4K jobs away from its all-time high achieved in October 2019 (50K).

- As for architectural services, the industry reached an all-time high in November (201.3K).

- Producer Price Changes (as of December 2021):

- Lumber (softwood) increased 8.6% over the last 12 months (up 48.8 percentage points from September)

- Flooring increased 16.5% over the last 12 months (down 1.5 percentage points from September)

- Textiles & Fabrics increased 21.8% over the last 12 months (up 5.2 percentage points from September)

- Furniture – residential increased 13.6% over the last 12 months (up 2.6 percentage points from September)

- Cabinetry increased 5.0% over the last 12 months (up 2.1 percentage points from September)

- Paint increased 14.3% over the last 12 months (up 3.5 percentage points from September)

*Note: Any score above 50 represents expansion (i.e., growth) and below 50 represents contraction (i.e., decline).

Categories

Interior Design Billings Index (IDBI)